Buy Now, Pay Later (BNPL) is no longer just a novelty at checkout. It is increasingly designed to feel native to the payment flow, especially online. Globally, Chargeflow estimates BNPL reached about $560.1 billion in 2025 GMV, up 13.7% year over year. The same source places provider revenue at $44.89 billion in 2025 and $54.56 billion in 2026, showing how earnings differ from transaction volume. Adoption is also broadening: global BNPL users reached about 380 million in 2024 and are projected to grow to around 670 million by 2028. Vietnam’s checkout changes sit inside this wider shift toward installment options that are fast, digital, and integrated where people already shop.

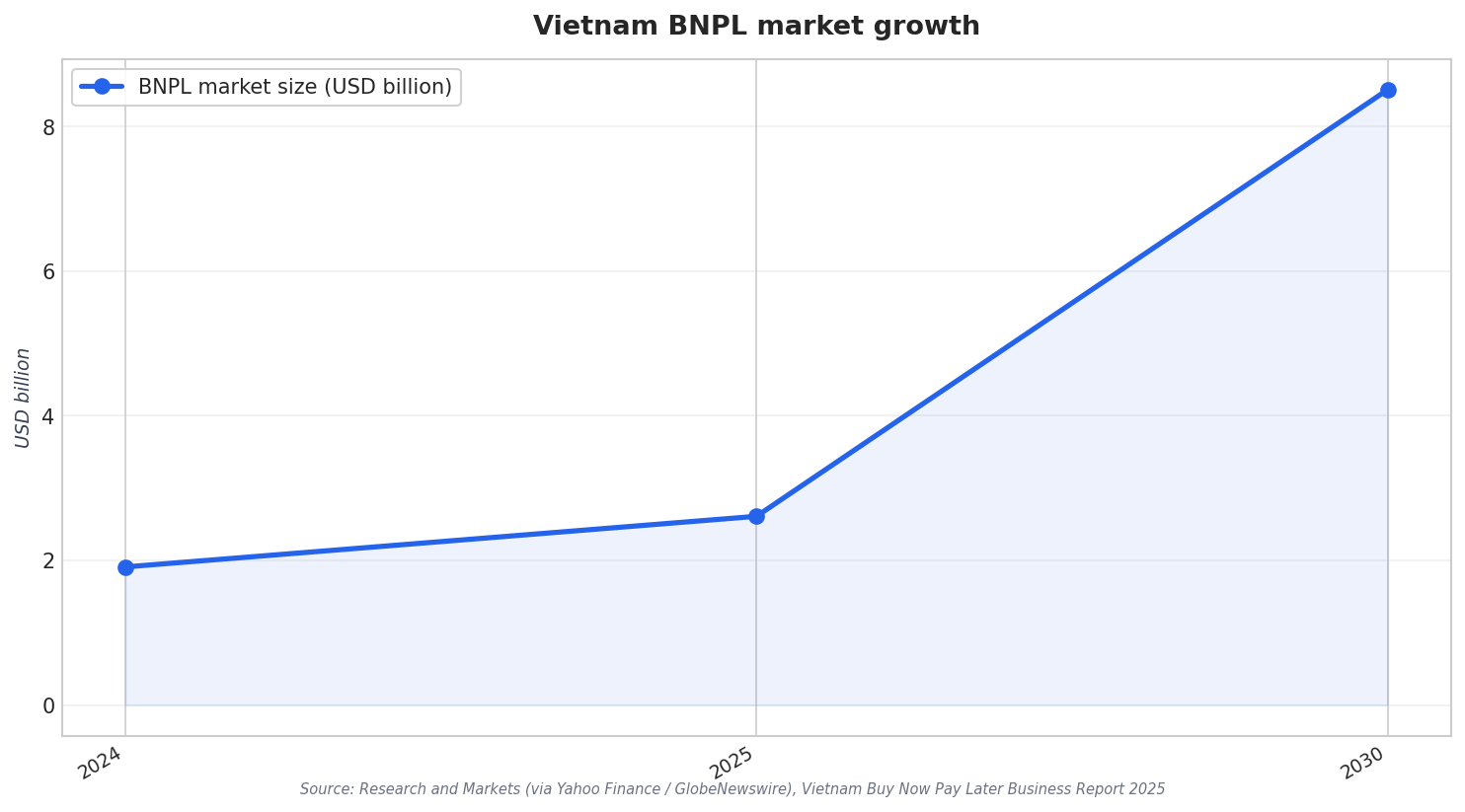

In Vietnam, the BNPL story is being pulled forward by both demand and access. Research and Markets projects the BNPL payment market in Vietnam will grow 36.5% in 2025 to reach US$2.61 billion. The same report says the market achieved a CAGR of 58.3% from 2021 to 2024 and forecasts a CAGR of 26.7% from 2025 to 2030. By the end of 2030, it projects expansion from a 2024 value of USD 1.91 billion to about USD 8.51 billion. Elevate Pay highlights a key backdrop for why installments can resonate: it states that less than 6% of Vietnam’s population possesses credit cards, positioning BNPL as an alternative for flexible financing.

Why BNPL Checkout Is Becoming the Default Flow

The biggest “revolution” is not only new lenders. It is the way installments appear at the point of payment. Mordor Intelligence describes embedded checkout as a standard pattern, presenting installments natively and reducing friction and time from selection to approval. It also notes that API-first providers can shorten deployment cycles and unify approval routing across multiple lenders in a single flow. That matters because it makes BNPL activation a low-effort lever for merchants. Chargeflow also frames the merchant impact in performance terms, stating BNPL can increase average order value (AOV) by 20–40% and improve conversion rates. In Vietnam, those mechanics connect to what Elevate Pay calls the dominance of the online channel, driven by e-commerce platforms embedding BNPL at checkout.

Mainstream adoption also depends on distribution: where BNPL appears and who promotes it. Research and Markets points to players such as Atome and Kredivo targeting younger, tech-savvy consumers, and it cites partnerships with major retailers such as Pharmacity that embed BNPL into everyday transactions. The same report says integration into super apps like MoMo and ZaloPay is boosting accessibility and adoption across income groups, while expansion into offline retail and non-retail sectors like education and travel reflects diversification beyond classic e-commerce. Mordor Intelligence adds that installments are moving beyond native e-commerce checkout into stores through virtual cards, physical cards, and contactless acceptance at terminals, extending BNPL into card-present settings.

As the Vietnam buy now pay later BNPL market grows, risk and oversight become part of the mainstream conversation. Chargeflow reports global BNPL default rates (charge-offs) of roughly 1.8%–2%, but also notes that about 34%–41% of users report making at least one late payment. Separately, The Motley Fool reports that over 25% of Americans regret using BNPL due to unexpected costs, a reminder that user experience can cut both ways depending on disclosure and budgeting. In Vietnam, Research and Markets flags regulatory developments, including a proposed sandbox by the State Bank of Vietnam, signaling an emerging framework aimed at consumer protection and market stability as competition and innovation accelerate.

How fast is Vietnam’s BNPL market projected to grow through 2030?

What is driving BNPL adoption at checkout in Vietnam?

What do sources say about the business impact of BNPL for merchants?

What risks are associated with BNPL as it goes mainstream?

What is happening with oversight and regulation around BNPL in Vietnam?